Barrier option pricing within the Black-Scholes model in C++

Aims

- analytical barrier pricing functions within the Black-Scholes model

- single and double barriers, continuous barriers/barriers at maturity, barrier and touch options

- analytical calculation of price sensitivities (Greeks)

- C++ in a functional form so it could be quickly ported to C

Source Code

The source code is released under the

GPLv2

or above:

Usage

// put/call option

price = bs::putcall(S,vol,r,rf,T,K,pc);

delta = bs::putcall(S,vol,r,rf,T,K,pc,bs::types::Delta);

// barrier option, knock in/out, barrier continuously observed or at maturity only

price = bs::barrier(S,vol,r,rf,T,K,B1,B2,rebate,pc,kio,bcont);

vega = bs::barrier(S,vol,r,rf,T,K,B1,B2,rebate,pc,kio,bcont,bs::types::Vega);

// binary option: cash or nothing (domestic), asset or nothing (foreign)

price = bs::binary(S,vol,r,r,T,B1,B2,fd);

// touch/no-touch option

price = bs::touch(S,vol,r,rf,T,B1,B2,fd,kio,bcont);

// probability that the asset at maturity S_T is in-the-money (irrespective of the path and if it may have hit a barrier before)

prob = bs::prob_in_money(S,vol,mu,T,K,B1,B2,pc);

// probability that the asset S_t hits any of the barriers at any time in [0,T]

prob = bs::prob_hit(S,vol,mu,T,B1,B2);

// Note, if any of the barriers B1 or B2 are set to zero then it is assumed that barrier does not exist.

// Therefore, barrier() can also price vanilla put/call options and touch() can also price cash/asset-or-nothing options.

// putcall(), binary(), bincash(), etc are still provided for convenience.

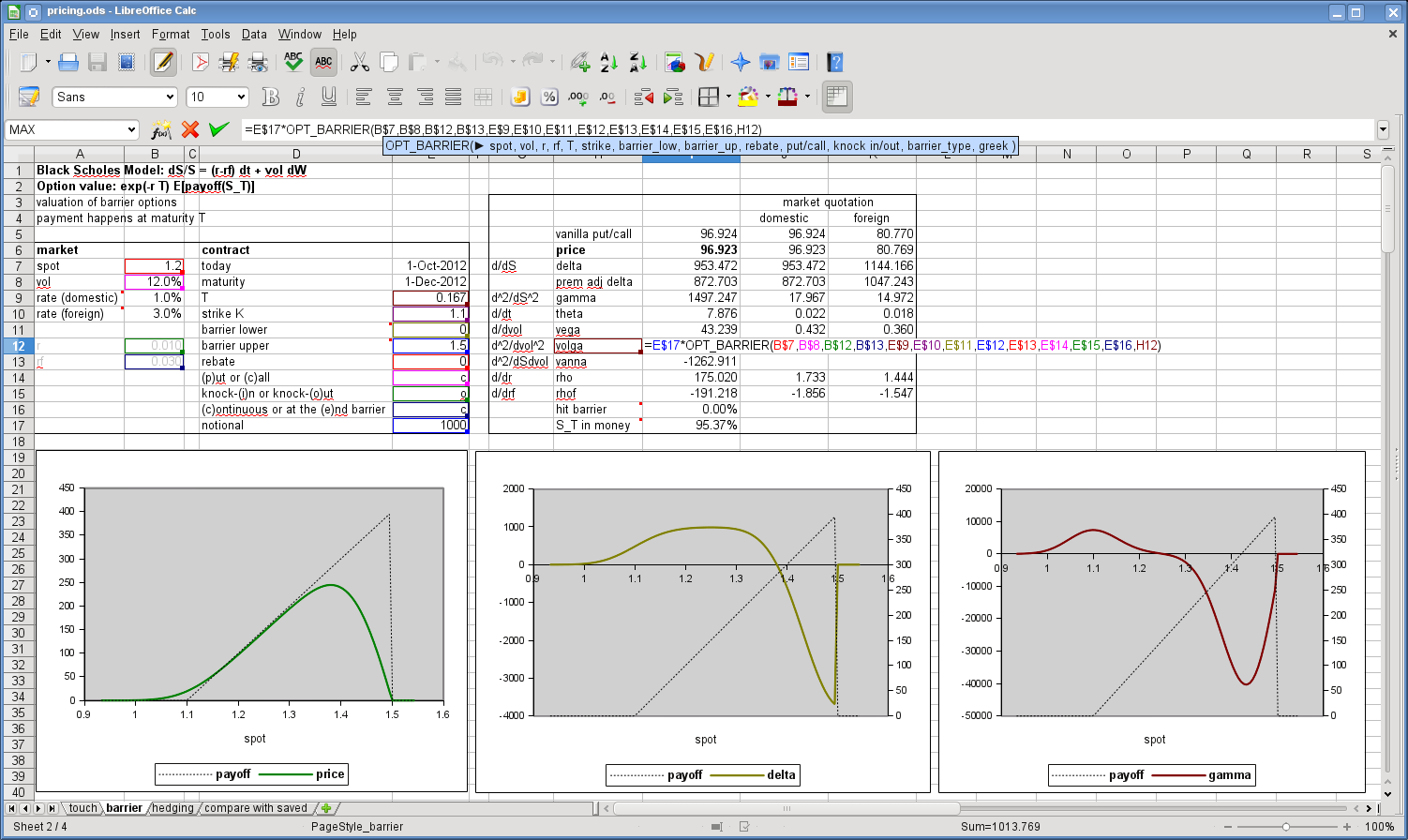

Spreadsheet integration

The main barrier pricing functions have been integrated into

LibreOffice since version

4.0.

They are available as OPT_BARRIER() and OPT_TOUCH().

Unfortunately,

gnumeric maintainers

were not so keen and the code

did not get included.

Benchmark

The benchmark below shows the number of cpu-cycles used by each pricing

function. These numbers are approximate and cpu-architecture-

and input parameter dependent.

Here it is run on an Intel Core i5-750

Nehalem. The first three functions are only for comparison and the first

function gives an idea about the overhead of the benchmark

(dummy always returns 0) due to virtual function calls, etc.

$ ./bench 2667 1000 # this cpu clocks at 2.667GHz, run 1000k loops

number of cpu-cycles per function:

price delta gamma theta vega volga vanna rho rho_f

dummy 10 10 10 10 10 10 10 10 10

add 11 11 11 11 11 11 12 11 11

norm cdf 48 49 48 48 48 48 48 48 48

bincash() 299 355 357 505 355 356 357 395 360

binary() 318 373 374 520 371 370 377 413 375

1 touch() 983 1414 1808 1384 1506 2134 2412 1619 1528

2 touch() 15930 21079 26884 22407 37250 66878 54912 42026 37791

putcall() 393 263 316 1102 837 844 851 895 891

T barrier() 1312 1634 1537 2124 1520 1540 1542 1617 1615

1 barrier() 3542 6202 8027 5797 5890 8041 10173 6105 6301

2 barrier() 27245 37057 44508 46825 71090 128084 105030 76324 76943

Source:

Compile as follows:

$ g++ -Wall -O2 bench.cpp -o bench.o

$ g++ bench.o bs.o -o bench

Examples

#include <cstdio>

#include <cstdlib>

#include "bs.h"

int main(int argc, char** argv) {

// define market data

double S=1.0, vol=0.15, r=0.03, rf=0.01;

// define call option

double T=1.0, K=1.0;

bs::types::PutCall pc = bs::types::Call;

// define barrier option (up-and-out)

double B1=0.0, B2=1.2, rebate=0.0;

bs::types::BarrierKIO kio = bs::types::KnockOut;

bs::types::BarrierActive bcont = bs::types::Continuous;

double price, delta, prob, bhit;

// calculate call option price

price=bs::putcall(S,vol,r,rf,T,K,pc);

delta=bs::putcall(S,vol,r,rf,T,K,pc,bs::types::Delta);

prob=bs::prob_in_money(S,vol,r-rf,T,K,0.0,0.0,pc);

printf("call option: price = %f, delta = %f\n", price, delta);

printf(" probability of S_T in the money = %.2f%%\n\n", prob*100.0);

// calculate barrier option price

price=bs::barrier(S,vol,r,rf,T,K,B1,B2,rebate,pc,kio,bcont);

delta=bs::barrier(S,vol,r,rf,T,K,B1,B2,rebate,pc,kio,bcont,bs::types::Delta);

prob=bs::prob_in_money(S,vol,r-rf,T,K,B1,B2,pc);

bhit=bs::prob_hit(S,vol,r-rf,T,B1,B2);

printf("barrier option: price = %f, delta = %f\n", price, delta);

printf(" probability of S_T in the money = %.2f%%\n", prob*100.0);

printf(" probability of hitting the barrier = %.2f%%\n\n", bhit*100.0);

return EXIT_SUCCESS;

}

Compile:

$ g++ -c -Wall -O2 bs.cpp

$ g++ -c -Wall -O2 demo.cpp

$ g++ demo.o bs.o -o demo

$ ./demo

call option: price = 0.068926, delta = 0.576720

probability of S_T in the money = 52.33%

barrier option: price = 0.019619, delta = 0.023680

probability of S_T in the money = 39.97%

probability of hitting the barrier = 24.04%

Another example compares the analytical results of the price

sensitivities vs finite difference approximation:

Maths

Unfortunately, gnumeric maintainers

were not so keen and the code

did not get included.

Unfortunately, gnumeric maintainers

were not so keen and the code

did not get included.